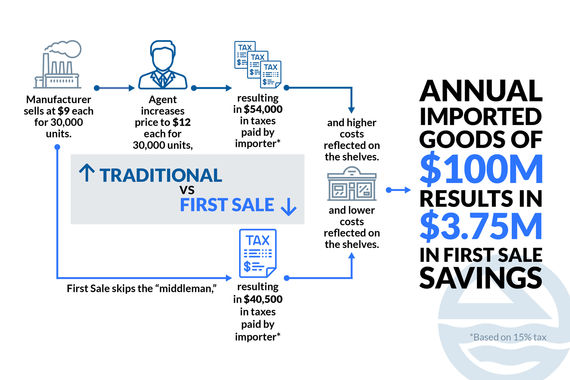

Straight from the source. That’s a term we like to see when purchasing our bottled water, or something we seek to hear from our server during that farm-to-table dining experience. Yet when it comes to importers, the First Sale rule can have a much larger impact than the feel-good appeal of locally sourced kale. It can mean a huge financial saving for retail supply chain importers if they go straight to the source, or manufacturer of goods, to buy directly and invoke the First Sale rule.

The First Sale Rule is one which allows importers to use the price paid in the first, or earlier sale, as the basis for customs duty to be paid. Many importers purchase at the second sale, from a middleman vendor who serves as the go-between from the manufacturer to the importer. This second sale is a marked up price. Paying duties on a lesser, first sale price, presents a tremendous savings opportunity, not only for the textiles and footwear supply chain industries where apparel and sneakers are subject to higher duty rates but also for manufacturing, electrical equipment, machinery, food and agriculture, and others. The bottom line, if you are purchasing from a trading company or sourcing agent, there may likely be an opportunity to take advantage of first sale pricing.